India's Data Center Market at a Glance

India's data centre market has quadrupled from 350 MW to approximately 1.5 GW in six years, with a further 3.8 GW under construction or in advanced planning. Three hyperscalers — AWS, Microsoft, and Google — have collectively committed $45.2 billion in cloud and data centre infrastructure since October 2024, signalling a phase transition from opportunistic deployments to strategic, decade-long infrastructure bets. Vacancy rates in core markets have compressed to 4.3%, well below the APAC average, confirming structural undersupply. This chapter maps the forces driving the boom, quantifies execution risk by hyperscaler, examines geopolitical tailwinds from MENA instability, and presents scenario-weighted projections through 2030. The central finding: India's binding constraint is not demand but supply — specifically power grid capacity, water infrastructure, and regulatory throughput.

A Market That Has Outrun Every Forecast

Something shifted in India's data centre industry in 2025. Double-digit growth had been routine since 2020; the 2025 shift was a change in scale of conviction. In a span of weeks between October and December 2025, AWS, Microsoft, and Google collectively pledged $67.5 billion in cloud and data-centre infrastructure for India — eighty percent of those commitments arriving in December alone (Washington Post, The AI spending frenzy reaches India· Washington PostDec 2025). Of that, roughly $45.2 billion is the data-centre slice (AWS $12.7 B + Microsoft $17.5 B + Google $15 B); Amazon's broader $35 B India figure spans retail, logistics, and consumer fintech beyond pure cloud.

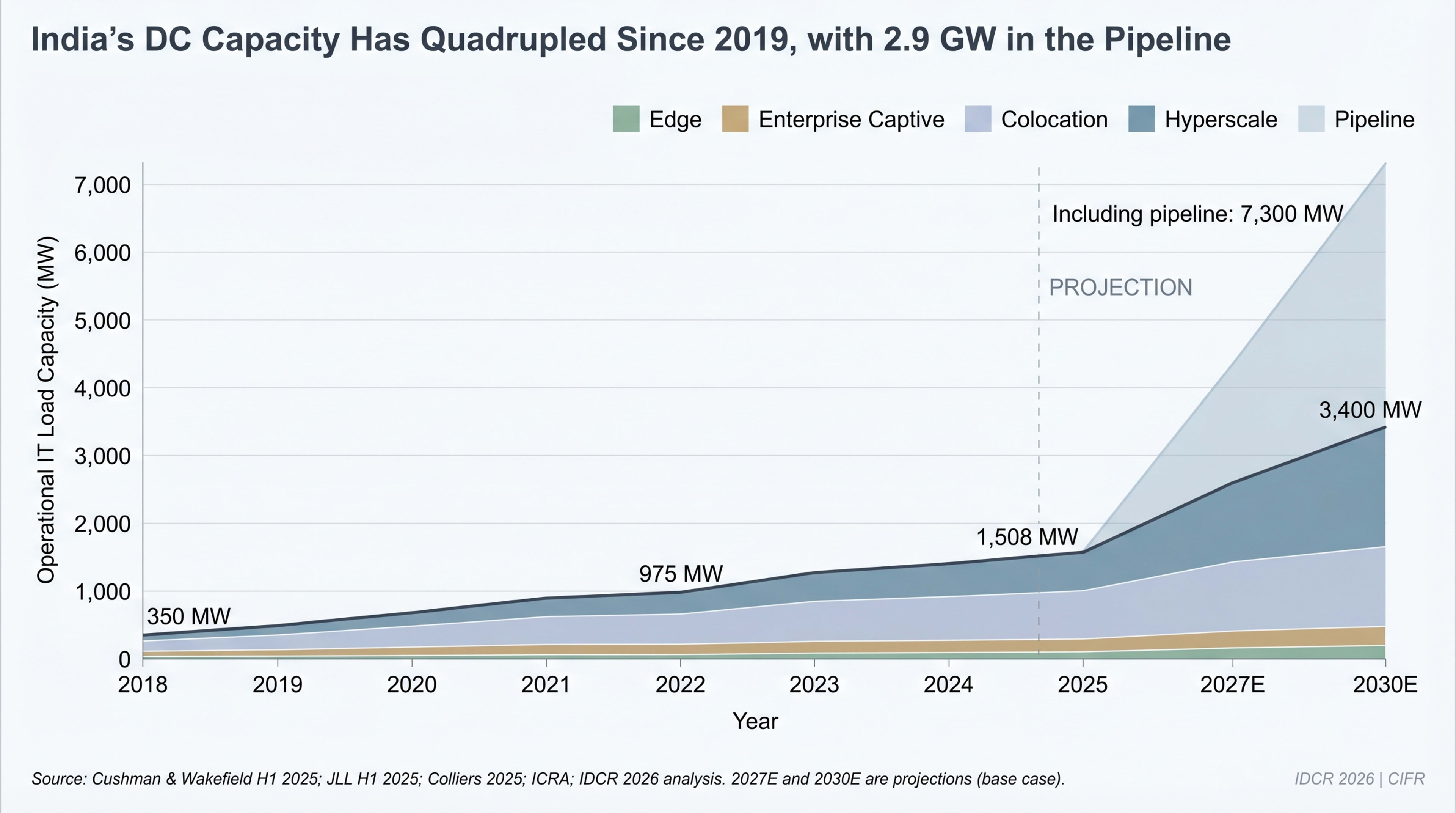

The numbers confirm the momentum. India's total operational IT load reached ~1,520 MW by end-2025 per JLL's H1 2025 India Data Centres dynamics· JLLH1 2025; Cushman & Wakefield's narrower colocation methodology· Cushman & Wakefield2025 places the figure at approximately 1,300 MW. Either way, capacity has roughly quadrupled from the ~350 MW baseline of 2018-19 — a CAGR exceeding 25%. The cross-check from CBRE's 2026 outlook· CBRE2026 projects 1.7–2.0 GW operational by year-end on $30 B of fresh deployment, with 500 MW of new supply landing in 2026 alone (CBRE via Business Today· Business TodayApr 2026).

Pipeline visibility through 2030 stands at approximately 3.8 GW under construction or in advanced planning. If executed on schedule, India's installed base would exceed 5.3 GW by end-2030, placing the country among the top three Asian markets after mainland China and Japan. The execution lag has compressed from 24 months in 2023 to 18-24 months today; faster, but still well outside the 12-month metronome that hyperscalers run elsewhere. Live snapshots of grid load and fuel mix that frame DC build-out are tracked across India Energy Atlas state pages; the data-centres dashboard aggregates them at a national level.

Why 2025 Became an Inflection Point

Three structural factors converged:

- US–China decoupling narrative. US cloud providers face political pressure to reduce exposure to TSMC fabs and PRC manufacturing. India positions as a politically acceptable alternative for AI compute, soft-hosted cloud, and edge workloads. AWS's prior $3.7 B India footprint anchors an additional $12.7 B by 2030 committed in late 2025 (CNBC, AWS Q1 2026· CNBCApr 2026).

- Talent and regulatory arbitrage. India's all-in cost structure (power, cooling, labour) is 40-50% below Singapore for equivalent colocation. Layered on top, India's data-localisation mandates — RBI payment-systems rules, the DPDP Act 2023, and the IT Rules 2021 amendments — require operators serving Indian users to host domestically. Compliance mandates capacity, which justifies hyperscaler investment.

- Global AI inference boom. Training centralised (mostly US); inference distributed (everywhere). India's population, e-commerce density, and fintech base create the world's largest single-language inference market. Google's December 2025 announcement bundled $15 B of AI infrastructure with the America-India Connect subsea programme to Singapore, South Africa, and Australia; it also confirmed a gigawatt-scale Adani-partnered campus in Visakhapatnam plus expansions in Noida (Business Today, Apr 2026· Business TodayApr 2026).

Grid carbon intensity is also more favourable than the headline coal-share suggests. Live national average is currently , well within the band that lets hyperscalers pursue carbon-neutral narratives via on-site solar PPAs and renewable open-access procurement. The India Energy Atlas carbon-intensity dashboard publishes the same series at hourly resolution.

Keep reading — free, takes 30 seconds

India's Data Center Market at a Glance continues with 1,899 words and 8 figures.

Free Clerk account. No card. We use it to remember your reading position and unlock subscriber chapters.